Introduction: Context of Inflation and Oil Price Spike

The recent escalation of conflict in the Middle East has led to a significant spike in oil prices, reigniting inflationary pressures across global economies.

Energy costs are a critical input for many sectors, and sharp increases tend to ripple through supply chains, pushing consumer prices higher.

For investors, this renewed inflation threat underscores the importance of incorporating effective inflation hedges into portfolios. Inflation-linked exchange-traded funds (ETFs) have become a popular tool for managing inflation risk, offering exposure to assets designed to preserve purchasing power in inflationary environments. This article explores how inflation ETFs can be used strategically in the current macroeconomic context.

A Brief History of Inflation ETFs

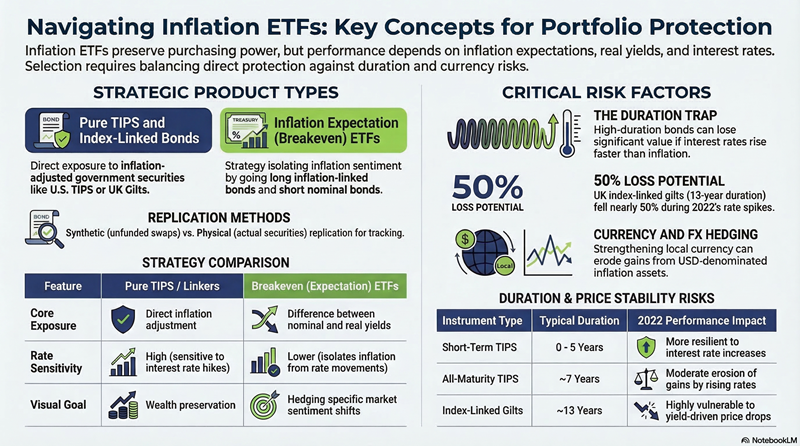

Inflation ETFs emerged in response to growing investor demand for accessible tools to hedge against rising prices. The first inflation-linked ETFs were launched in the mid-2000s, primarily focused on US Treasury Inflation-Protected Securities (TIPS). These early products offered retail and institutional investors a liquid way to gain exposure to inflation-adjusted bonds without directly purchasing individual securities.

As inflation concerns intensified during the late 2000s and early 2010s, particularly following the Global Financial Crisis and subsequent quantitative easing programs, the market for inflation ETFs expanded. Providers began launching ETFs tied to various inflation benchmarks, including breakeven inflation rates and inflation swaps. European markets followed suit, introducing ETFs linked to UK index-linked gilts and Eurozone inflation-linked bonds.

Today, the inflation ETF landscape spans a wide range of strategies, from pure plays on inflation expectations to diversified baskets of inflation-protected securities. These products have evolved to meet the needs of both domestic and international investors, offering currency-hedged variants and thematic exposures. Their growth reflects a broader recognition of inflation as a persistent risk in modern portfolios.

Lessons from the 2022 Inflation Environment

The inflation surge of 2022 was driven by a confluence of post-pandemic demand recovery, supply chain bottlenecks, and geopolitical shocks, culminating in a rapid and aggressive tightening cycle by central banks worldwide. During this period, inflation ETFs played a pivotal role in helping investors navigate the changing landscape, with inflation themed ETFs being one of the few exposures in Fixed Income that provided positive returns over the year of 2022 (besides money market).

At first glance, inflation-linked bonds, like TIPS in the US or inflation-linked gilts in the UK, seem like the obvious choice to protect against inflation. But during the year of 2022 interest rates increased sharply often eroding some or all of the gains from the increase in inflation. In times of a rate rising environment, inflation-linked bonds with a shorter duration are preferable. For example, there are ETFs that provide exposure to TIPS with a 0 to 5-year or 0 to 10-year maturity. Still, even those didn’t fair that well in 2022, increasing in performance first, but when rates started to increase more, the increase in rates still eroded the gains from inflation.

Enter inflation expectation ETFs. These ETFs track inflation swap rates and mirror the shifts in market sentiment more closely. In effect they provide an exposure that is long the inflation-linked bonds and short government bonds of similar maturity. As central banks signalled increasingly hawkish policies, these ETFs experienced heightened volatility, reflecting the market’s evolving view on future inflation, but they were the ETFs that best provided a protection against inflation erosion.

Performance of different US inflation ETFs for the year of 2022 (in USD).

Performance of different US inflation ETFs for the year of 2022 (in USD).

In the UK, index-linked gilt ETFs faced even stronger headwinds, with real yields climbing and suppressing returns despite rising inflation. Investors learned that while inflation protection is valuable, it doesn’t insulate against all risks, particularly those tied to interest rate movements.

This effect was much more exacerbated by the much higher duration of UK inflation-linked ETFs, which is around 13 years, compared to the duration for a typical all-maturity TIPS ETF at round 7 years. The iShares Inflation Linked Gilts ETF was down nearly 50% at the end of September 2022 from the beginning of the year. Thus, the interplay between inflation expectations, real yields, and monetary policy became a defining feature of the 2022 experience, shaping how investors approach inflation hedges today.

Performance of a UK inflation ETF for the year of 2022 (in GBP).

Performance of a UK inflation ETF for the year of 2022 (in GBP).

What’s Different in the Current Environment?

While the inflationary pressures of 2022 were largely driven by monetary and fiscal stimulus, the current environment is shaped more by supply-side shocks, particularly the recent spike in oil prices due to geopolitical tensions in the Middle East. And unlike the steady march of rate hikes seen in 2022, central banks today appear more cautious, with many currently on hold with rate cuts but not quite in tightening cycles either.

This shift has altered the dynamics for inflation ETFs. With inflation expectations becoming more volatile and tied to geopolitical risk, nominal inflation expectation ETFs may see greater swings as markets react to headlines. At the same time, real-yield-sensitive ETFs like TIPS may benefit from a stabilization in real interest rates, especially if growth concerns temper central bank hawkishness. On the other hand, if inflation persists it may trigger a set of rate hikes which can be very detrimental to any ETF with a longer duration. Therefore, I’d probably still prefer ETFs with shorter maturities or the inflation expectation ETFs.

Currency Considerations for non-US Investors

For investors based in the UK or other European countries, currency exposure adds another layer of complexity when investing in USD-denominated inflation ETFs. While these products offer access to robust inflation-linked markets like the US TIPS sector, they also introduce foreign exchange risk that can significantly affect returns.

When the pound or Euro weakens against the dollar, the value of USD-denominated assets rises in GBP/EUR terms, potentially enhancing returns. Conversely, a strengthening pound/Euro can erode gains, even if the underlying inflation protection performs well. This dynamic means that investors must weigh the benefits of inflation hedging against the risks of currency fluctuations.

Some ETF providers offer currency-hedged versions of their inflation products, which aim to neutralize FX exposure. However, these come with additional costs and may not perfectly offset currency movements. Alternatively, investors can opt for inflation ETFs denominated in their local curreny, such as those tracking UK index-linked gilts or Eurozone inflation bonds, to avoid FX risk altogether. While these products are aligned with domestic inflation trends, they come with a high duration and may not offer the same diversification or depth as their USD counterparts.

Ultimately, the choice depends on an investor’s view of currency direction, risk tolerance, and portfolio objectives. A blended approach, combining hedged and unhedged positions, may offer a balanced strategy for navigating both inflation and FX risk.

Irene Bauer