We have spent decades in investment management trying to solve the same fundamental problem: information asymmetry. It used to be about who had the data, but in an era of total transparency, the struggle has shifted. Today, the real constraint is the ability to process that data consistently, objectively, and at scale. Whether an advisor is outsourcing to a Discretionary Fund Manager or building bespoke models with ETFs and funds, most firms are still operating within a structural limitation defined by human bandwidth. We have historically settled for quarterly reviews and monthly factsheets not because they represent the optimal frequency for oversight, but because they were the only cadence that was operationally realistic for a human team to execute.

What is changing in 2026 is that this constraint is no longer binding. We are moving beyond the era of assistive AI-tools that help us write, summarize, or search - entering a period defined by autonomous systems that continuously monitor, test, and challenge our investment decisions. This shift is subtle in its description but profound in its impact, representing a move from periodic snapshots to a state of continuous, event-driven intelligence.

From Passive Assistance to Autonomous Execution

The transition from assistance to autonomy is the defining characteristic of this Agentic Moment. Most of the AI tools advisors have experimented with over the last few years have been passive; they are useful, certainly, but they remain entirely dependent on a human asking the right question at the right time. Agentic systems invert that model. Instead of waiting for a prompt, they operate against a defined set of rules, thresholds, and objectives, scanning for conditions that require attention. In practical terms, this means plugging into the core plumbing of an investment process - portfolio data, fund information, and model structures - then interrogating it without fatigue.

The power of this shift lies in the ability to encode an investment philosophy into something executable. Every advisor has implicit rules regarding what constitutes acceptable underperformance, how much style drift is tolerable, or what specific events break an investment case. Historically, these rules have lived in the knowledge bank of the investment committee or in loosely documented notes. Agentic systems force a firm to make these rules explicit, and once they are codified, they can be applied with a level of consistency that human oversight simply cannot match.

Raising the Resolution of Investment Oversight

This effectively raises the resolution of investment oversight. In the traditional model, issues tend to be identified after they have already had a measurable impact on performance. A fund underperforms, a portfolio behaves unexpectedly, and the subsequent analysis is almost entirely retrospective. With agentic monitoring, the system is looking for precursors rather than outcomes. It can detect when a manager’s behaviour begins to deviate from their stated style, when portfolio exposures start drifting away from their intended design, or when the interaction between holdings changes in a way that alters the risk characteristics of the entire model.

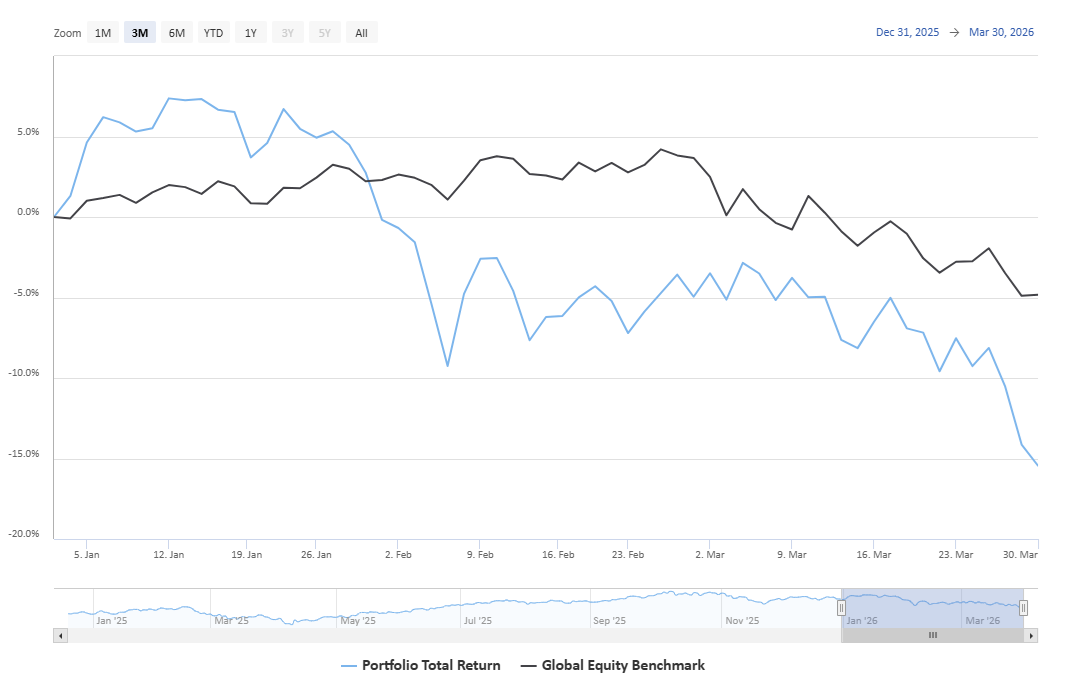

Figure 1 – The 2026 YTD losses shown for a portfolio built using a 100% weighting to Themed ETFs

Crucially, this is not just about generating more alerts. A poorly designed system will simply create more noise, leading to alert fatigue. The real value comes from structured interpretation—linking a signal to a potential implication. Identifying that a fund has moved into the bottom quartile over six months is a trivial task for any database. Understanding whether that move reflects a temporary factor headwind or a fundamental breakdown in the manager’s process is where the analytical burden sits. This point is illustrated in Figure 1 above—being alerted about large losses is one thing; knowing why they are occurring is a different matter entirely. Well-designed agents begin to replicate the kind of thinking one would expect from an experienced analyst, connecting disparate data points rather than just surfacing them.

Challenging the Black Box of Delegation

For those working with DFMs, the implications are arguably even more significant. Outsourcing has always involved a trade-off between efficiency and transparency. You gain access to institutional capability, but you lose a degree of visibility, becoming dependent on the manager’s own reporting and narrative. Agentic oversight reduces that dependency. By independently analysing DFM portfolios at the holdings and factor level, advisors can form their own objective view of what is happening beneath the surface.

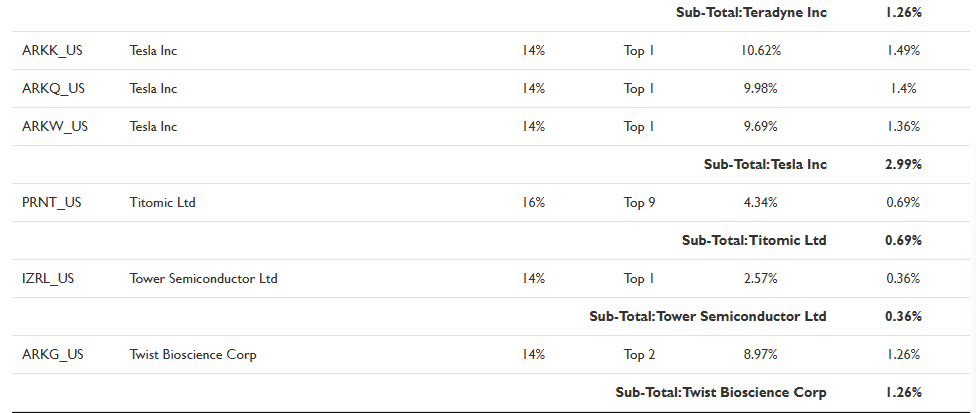

Figure 2 – The stock holdings aggregated across a portfolio built using a 100% weighting to Themed ETFs

Figure 2 above lists the aggregated holdings across all the ETFs allocated in the portfolio—it is only at this level of granularity that one can fully understand the drivers of the returns of the overall investment. This allows for a much clearer picture of consistency over time, identifying whether portfolio changes align with the stated philosophy or if risks are being introduced implicitly through episodic positioning.

However, it is worth being clear that this is not a free upgrade. Poorly implemented agentic systems can create a dangerous false sense of control. If the underlying rules are weak or the data feeds are incomplete, a firm simply ends up automating flawed oversight. In some cases, this is worse than doing nothing, as it creates a layer of overconfidence that can mask emerging risks. There is also the very real danger of over-intervention. When you move to continuous monitoring, you are exposed to far more signals, and the discipline required to

not act becomes even more important. The agent can surface patterns, but it does not carry professional accountability.

The Evolution of the Advisor’s & DFM’s Roles

This points to a gradual but meaningful change in the advisor’s role. We are moving from doing the analysis to supervising the system that performs it. The advisor becomes a supervisor of an intelligence layer rather than the primary engine of it. While that might sound like a loss of control, it is actually the opposite. You are not removing yourself from the process; you are repositioning yourself at the point where your input has the most impact. Clients are not paying for effort; they are paying for judgment. And judgment improves when it is supported by consistent, high-quality analysis that never sleeps.

There is also a significant regulatory and commercial undercurrent to this shift. As expectations around suitability and ongoing service continue to rise, the ability to demonstrate continuous oversight becomes an invaluable defensive asset. Being able to evidence that portfolios are monitored systematically and that risks are identified proactively moves the conversation beyond we review this regularly to something much more tangible. Commercially, this redefines what a scalable advice model looks like, allowing a firm to maintain—or even increase—analytical depth while scaling its client base.

To this we can also add the realisation that as an advisor, many of your end investors also have these same AI tools at their disposal. If the recent article published in Citywire’s New Model Adviser publication is anything to go by (see Figure 3 below), don’t be surprised if your own advice service comes under much more scrutiny.

Figure 3 – The benefits of AI tools apply to both sides of the negotiating table.

A New Standard for Professional Accountability

Ultimately, the firms that pull ahead will not be those using AI to write faster reports. They will be the ones that have quietly rebuilt the core of their investment process around continuous, systematic oversight. This requires more than just adopting a new tool; it requires articulating an investment philosophy with enough precision that a system can execute against it. If it is now possible to monitor portfolios continuously and detect issues before they fully emerge, the central question for the industry is no longer technological, but professional: on what basis do we continue to rely on the periodic snapshot? Over the next few years, that question will become increasingly difficult to ignore.

Until next time.

Allan Lane