Why discretionary fund managers are quietly running the same trade twice - and how to fix it.

There are two artificial intelligence conversations happening in our industry today, and the failure to distinguish between them is creating a massive, unpriced risk. The first conversation is AI-as-an-investment-subject, the question of what we own. This is the loud, public debate about Nvidia's valuation, the durability of hyper-scaler capex, and whether the AI Seven are a bubble or a new paradigm. The second is AI-as-an-investment-process, the question of how we work. This is a quieter, more technical conversation about LLMs, agentic research, and the automation of the investment committee.

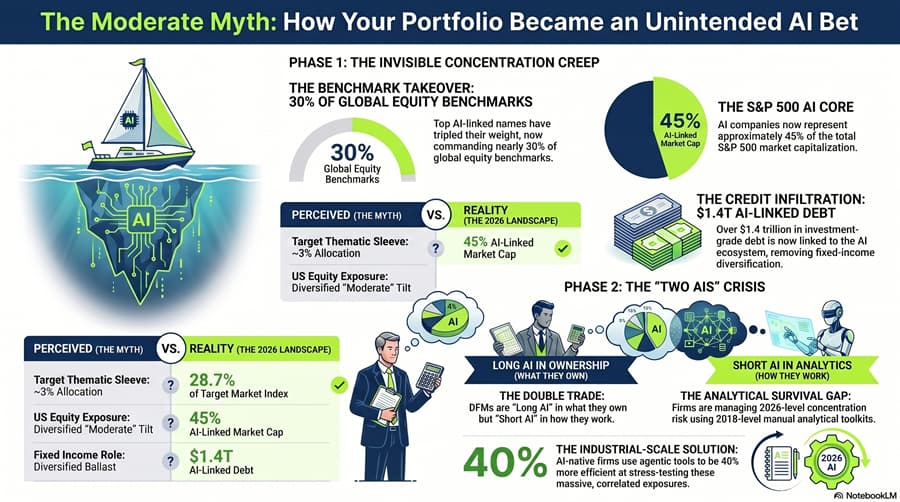

Figure 1 – The Moderate Myth: Most DFM firms are long AI in their portfolios while remaining short AI in their process - sleepwalking into 2026-level concentration risk with a 2018-level analytical toolkit.

Figure 1 – The Moderate Myth: Most DFM firms are long AI in their portfolios while remaining short AI in their process - sleepwalking into 2026-level concentration risk with a 2018-level analytical toolkit.

Most Discretionary Fund Manager (DFM) firms are currently long AI in their portfolios while remaining short AI in their process. They have sleepwalked into 2026-level concentration risk while relying on a 2018-level analytical toolkit. By solving these two problems in isolation, the industry may be arriving at the wrong answer twice.

The Moderate Portfolio's Secret Identity

The narrative of the moderate model portfolio has become a fiction. Most advisors would tell you they hold a diversified mix of assets with perhaps a small, 3–10% thematic sleeve for AI exposure. However, look-through analysis reveals a very different reality. Over the past decade, the weight of the major AI-linked names has tripled, now commanding nearly 30% of global equity benchmarks. When you add the fact that AI-linked companies represent almost half of the S&P 500's market capitalisation, a standard moderate portfolio with a typical US tilt is doing more thematic AI work than any satellite sleeve ever could. This is the total AI beta, and it is currently the most concentrated diversified bet in history.

The moderate portfolio of 2026 is, in truth, a high conviction, partially hedged bet on a correlated group of companies whose hardware depreciates faster than the infrastructure cycles of the past.

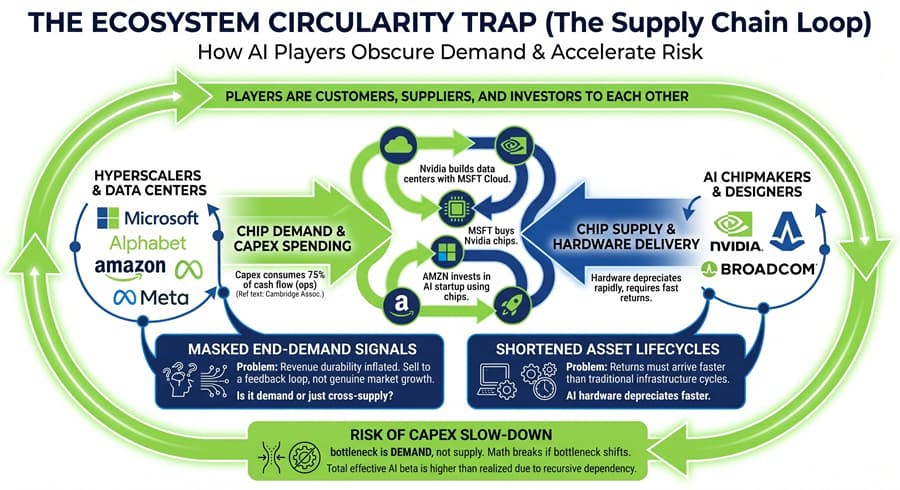

Figure 2 – The Ecosystem Circularity Trap: With over $1.4 trillion in investment-grade debt linked to the AI ecosystem and capex consuming 75% of cash flow, the fixed-income sleeve that should diversify a portfolio is now powered by the same fuel as the equity engine.

Figure 2 – The Ecosystem Circularity Trap: With over $1.4 trillion in investment-grade debt linked to the AI ecosystem and capex consuming 75% of cash flow, the fixed-income sleeve that should diversify a portfolio is now powered by the same fuel as the equity engine.

The risk is not just confined to the equity sleeve. The AI thesis has quietly infiltrated the credit markets, with over $1.4 trillion in investment-grade debt now linked to the AI ecosystem. For a DFM whose fixed-income allocation is anchored in broad benchmarks, the part that should diversify your portfolio is now increasingly powered by the same fuel as the engine. This creates a dangerous circularity. We are seeing a structure where the major players are simultaneously each other's customers, suppliers, and investors - a feedback loop that masks the moment true end-demand cools. When you consider that capital expenditure for these mega-cap spenders now consumes 75% of their cash flow, the self-funding narrative begins to look fragile.

The Process: Where the Real Alpha Lives

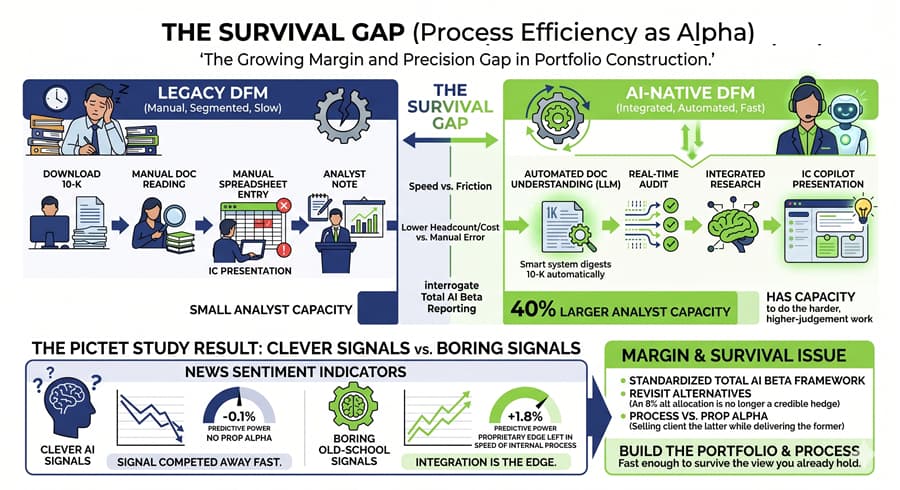

While the portfolio is becoming more concentrated, the process for managing it is undergoing a Darwinian shift. The common mistake is to hunt for AI alpha the idea that a Large Language Model can find a secret signal in earnings calls that the rest of the market has missed. The data suggests this is a fool's errand. A recent analysis of news sentiment indicators showed that clever AI signals had effectively zero predictive power over subsequent returns, while boring traditional momentum signals continued to do the heavy lifting. The edge in AI-as-a-process is not coming from novel signals; it is coming from industrial scale integration.

The real divide is opening between firms that treat AI as a magic box and those that treat it as a productivity layer. A DFM that builds an AI-native research factory where teams are 40% more efficient at processing primary documents and stress-testing portfolios effectively expands its analytical capacity without increasing headcount. This extra capacity is the only tool capable of solving the concentration problem. It allows a firm to interrogate the total AI beta across equity, credit, and alternatives in real-time. The firms winning this race are not those finding new data, but those using AI to understand the massive, correlated exposures they already hold.

The Double Trade and the Survival Gap

The reason the Two AIs Problem is a single crisis is that the allocators most vulnerable to AI concentration are typically the ones least equipped to measure it. We are seeing a double trade where legacy firms are running heavy, partially hedged thematic exposures using an outdated analytical toolkit. Meanwhile, the AI-native firms are using their process efficiency to aggressively de-risk or more accurately price that same exposure. They are using their speed to identify when ecosystem circularity is masking a demand peak, and they are adjusting their total AI beta accordingly.

Figure 3 – The Survival Gap: AI-native firms are using process speed to identify demand peaks and adjust their total AI beta, while legacy aggregators running the same double trade face business survival and margin compression risk.

Figure 3 – The Survival Gap: AI-native firms are using process speed to identify demand peaks and adjust their total AI beta, while legacy aggregators running the same double trade face business survival and margin compression risk.

The implications for the profession are no longer about thematic preferences; they are about business survival and margin compression. In a world where AI-generated signals are competed away instantly, the only proprietary edge left is the speed and cost of your internal process. A DFM that cannot put a single number on its total look-through AI exposure is no longer managing a portfolio it is hosting a hope-based strategy.

As the AI cycle inevitably tests the assumptions embedded in passive benchmarks, the industry will split. On one side will be the AI-native factories that understood what they owned. On the other will be the legacy aggregators who will have to explain to their clients why their moderate portfolio behaved like a tech-heavy hedge fund at exactly the wrong time.

The question isn't whether you have a view on AI; the question is whether you have built a process fast enough to survive the view you already hold.

Until next time.

Allan Lane